Bond Rally Stalls Ahead of Payrolls Report

Today’s Spotlight Market

Analysts are expecting the U.S. employment picture to have improved in January, after non-farm payrolls rose by a disappointingly anemic 74,000 in December.? The private sector employment report compiled by ADP and Moody?s Analytics showed that 175,000 jobs were added last month, with 160,000 of those jobs in the services sector. The widely-watched manufacturing sector shed 12,000 jobs according to the report. Traders are anticipating the Bureau of Labor Statistics to report that between 175,000 and 190,000 jobs were created in January, with the private sector accounting for about 160,000 of the increase. The unemployment rate is expected to remain steady at 6.7%, although much focus will be placed on the labor force participation rate, which has fallen to 35-year lows at 62.8%, with nearly 92 million Americans not in the labor force.

Fundamentals

Those pundits calling for the end of the historic U.S. Treasury Bond bull market have once again been proven wrong, as concerns over the growth prospects of emerging economies combined with uncertainly over U.S. job creation has kept investors interested in U.S. government debt as a ?safe haven? investment.? Bond prices have remained relatively firm, despite the continued tapering of Bond purchases by the Federal Reserve which announced a further reduction in Bond purchases of 10 billion per month to 65 billion per month last week. 30-year Bond yields which were approaching 4% for the first time since 2011 pulled back to 3.67% prior to the release of the January employment report. With current yields near the low end of the recent range (between approximately 3.50% and 3.98% since July), buyers may be hesitant to purchase Bonds at current levels — especially prior to an employment report that is expected to show an improvement in the employment picture from the end of 2013. However, should the jobs report once again disappoint, a test of 3.50% would not be out of the question. ?

Technical Notes? – View Today’s Chart

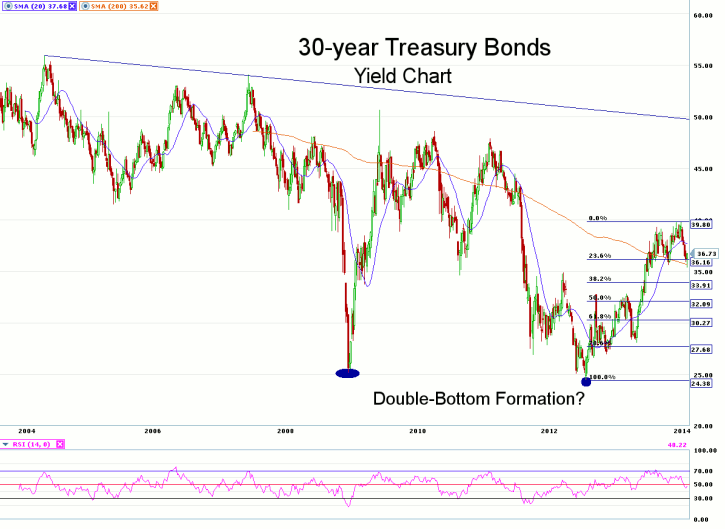

Looking at a weekly yield chart for the 30-year Treasury Bond for the past 10 years, we notice what appears to be a double-bottom formation as yields approached 2.5% back in late 2008, as well as again in the summer of 2012. Since the July 2012 lows, yields have rallied nearly 1.5%, but still remain well below the average highs of the past 10 years.?

If we chart the Fibonacci retracement from the July 2012 low to the recent high in yields, we note that 30-year yields have retraced about 23.6%. Should we see further ?flight to safety? buying or if the January payrolls report proves to be weaker than anticipated, a test of the 38.2% retracement is not out of the question, which would see yields fall below 3.40%, aided by stop orders being triggered should yields fall below psychological and technical support at 3.50%. It would take a move above 4.00% to reinforce the belief that the Bond bull market is on ?life support?.????

——————————————————————————————

Disclaimers

This article is provided for informational purposes only. No statement in this article should be construed as a recommendation to buy or sell a security or to provide investment advice. The content provided has been obtained from sources deemed reliable but is not guaranteed as to accuracy and completeness. optionsXpress makes every effort to provide timely information to its recipients but cannot guarantee specific delivery times due to factors beyond our control.

Derivatives involve substantial risk and are not appropriate for all investors. Please read the?“Disclosure Statement for Futures and Options”?prior to investing in futures or options.

For investments using a straddle or strangle options strategy the potential loss is unlimited. Multi-leg option strategies are subject to multiple commissions. Profits may be eroded by the commission expended to open and close the positions and?other risks?apply.