TWTR closed Friday trading at $64.50, up 1.6% with IV30? falling about one point. The?LIVEVOL? Pro Summary?is below.

Provided by Livevol

Twitter, Inc. (Twitter) is a global platform for public self-expression and conversation in real time. Twitter is a real-time platform, where any user can create a Tweet and any user can follow other users.?

This is a volatility note regarding earnings for TWTR and two quite surprising phenomena.

I wrote about TWTR in prior posts and how I saw what appeared a total mis-pricing of risk in the options (although that was unrelated to an earnings event). You can read that interesting tale by clicking on the title below:

Twitter (TWTR) – UPDATE: How the Option Market Totally Blew It, And We Knew it Two-Weeks Ago.?

But let’s focus on earnings volatility and the earnings event, which is due on 2-5-2014 AMC (aka Wednesday).

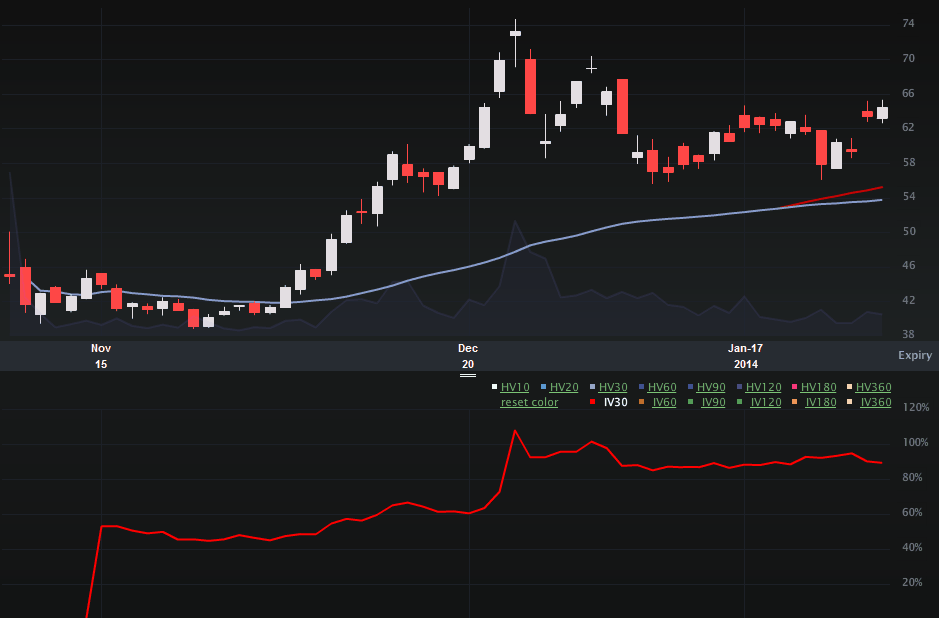

Let’s start with the Charts Tab (below). The top portion is the stock price, the bottom is the vol (IV30? – red vs HV20? – blue vs HV180? – pink).?

Provided by Livevol

Obviously there isn’t a lot of history for TWTR, but even in this short-time period we have seen the stock trade as low as $38.80 and as high as $74.73.? I’d say the equity market hasn’t quite reached equilibrium on this name yet and its first earnings report is going to be the beginning (not the end) of reaching that equilibrium.

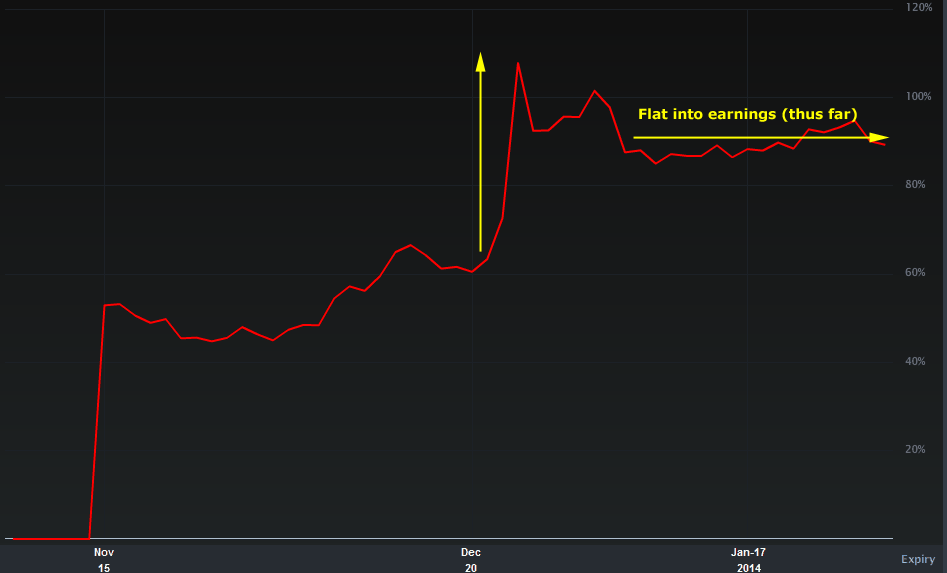

But ultimately, I want to examine the implied volatility, so let’s turn to the IV30? chart in isolation, below.

Provided by Livevol

Interestingly, the implied volatility has not been rising into earnings, but has actually been flat.? The rise in the implied occurred just after my original post which questioned, in simple terms, “what the? heck is TWTR vol doing trading so low?”

So, phenomenon number one that I want to point is simply that?the vol in TWTR has not been reacting to this upcoming event (it’s been flat).? But there’s a caveat here, and it’s a big one, I’m writing this article on Sunday afternoon. It would not surprise me if the vol starts climbing rather abruptly in to Wednesday’s close (the earnings date). I would in fact be surprised if TWTR implied does not go back to over 100% before the earnings release.

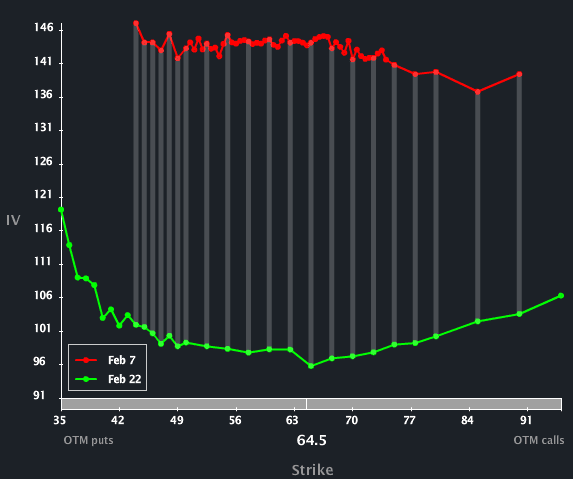

The second phenomenon I want to point out can be seen in the skew. The Skew Tab is included below.

Provided by Livevol

I have included the Feb 7 (weekly) and the Feb monthly options.? Obviously the Feb 7 weeklies are elevated to the Feb monthly vols b/c of earnings — by the end of trading on Wednesday, those Feb 7 options will represent essentially pure earnings vol and will be even more elevated.? So, the fact that the weeklies are elevated to the monthlies is?normal and expected.

My curiosity surrounds the size of that elevation.??

To read more about option skew and why it exists, you can read the post below:

Understanding Option Skew — What it is and Why it Exists?

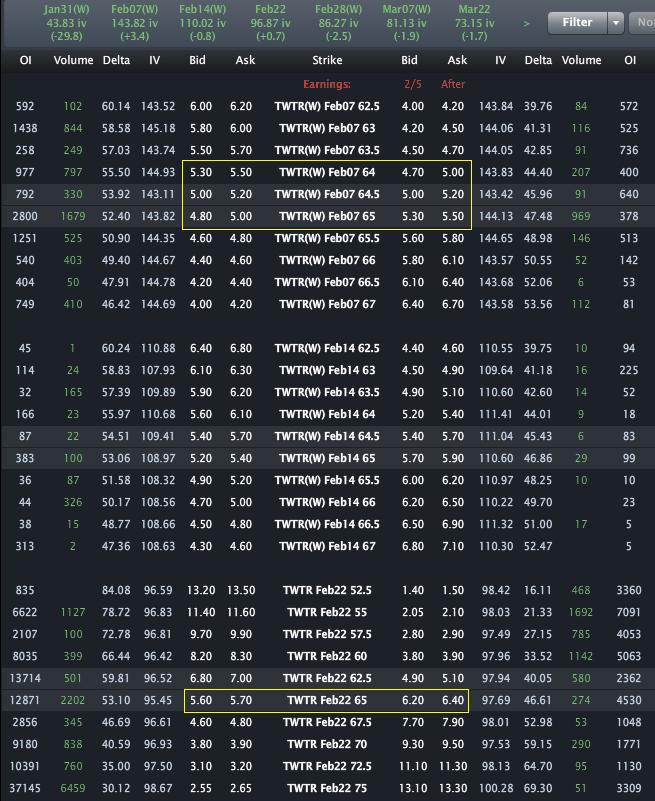

Finally, let’s look to the Options Tab (below) to put some numbers to that volatility difference.

Provided by Livevol

The Feb 7 weekly $65 strike straddle is priced to ~$10.30.? The Feb monthly $65 strike straddle is priced to ~$11.90.

So, basically, that means the time between Feb 7 and Feb 21 (Feb monthly expiration) is worth ~$1.60 on $65 strike straddle.? This implies (sort of) that whatever the move is off of earnings, the stick movement after Feb 7 but before Feb 21 is going to be pretty muted.

Why do I say “sort of”? Keep in mind that if the stock moves wildly away from $65 off of earnings, the vega (volatility dollars) in the Feb monthly $65 straddle will tend to zero as those options become deep in the money (far out of the money). If that happens, $1.60 will seem pretty expensive for just the volatility.? But if doesn’t… well, then it won’t…

Seriously,?this is trade analysis, not a recommendation.

In any case, let’s revisit TWTR and this article on Wednesday pre-earnings.? A lot can change in the next three trading days.