After a nice long climb to the top, the current market condition is reminiscent of corrections. Although there is a chance it could all work out and continue somewhat higher, the continuing decline of market breadth along with other indicators suggest we will soon be seeing more downside.

This week, right after a short strategy comment, we have another VIX suggestion, followed by an update for a previous VIX idea. Then after a long absence, we have a new Takeover File idea for Sprint Nextel Corp. (S).

?

Strategy

S&P 500 Index (SPX)

A quick retreat followed the new April 11 high of 1597.35 that took the index back to the upward sloping trendline where it then turned higher again last Friday. Since we are using a close below the March 19 low of 1538.57 as our trigger to implement the VIX hedge described in Digest Issue 13, with updates in both Digest Issue 14 and Digest Issue 15, the recent pull back came very close, reaching 1536.03 last Thursday before closing at 1541.6, but still above 1538.57. After finding support at the upward sloping trendline, it could continue somewhat higher to about 1574 forming a right shoulder of a potential Head & Shoulders Top. If so, 1538.57 would become the neckline setting the pattern off on the next decline.

E-mini S&P 500 Futures (ESM3)

As we pointed out last week, when the e-mini made a new high on Thursday April 11, open interest declined 968 contracts followed by another decline of 23,889 on Friday April 12. Last week through Thursday, the net decline was an additional 26,917 contracts. Declining open interest means the uptrend has become unstable as the longs are selling out and the shorts are closing hedges as they sell their long stock positions. When this many leave the party is probably over.

iShares Russell 2000 Index (IWM)

Following the conditional trade plan from last week, Thursday we booked the long put spread, the May 89 put with a short May 85 put, as IWM closed at 89.58 setting off a double top pattern with a minimum measuring objective back down at 85 or about a 10% correction.

With deteriorating market breadth and more evidence of long liquidation in the futures, we suggest hedging or exiting long positions, with perhaps the exception of special situations like iShares MSCI Japan Index (EWJ) 11.34 and Sprint Nextel Corp. (S).

?

Trading Volatility

Here is another suggestion from our friends at KeenOnTheMarket that fits nicely into our forecast that SPX could advance back up to 1574 over the next several trading days.

CBOE Volatility Index? (VIX)

Priced from the futures with a term structure that is currently in “contango” VIX options are unlike standard equity options. Contango is the term used to describe a term structure when the deferred prices are higher than the spot or front month price. The VIX has been in contango for quite some time with a relatively steep term structure.

However, in the past week the term structure flattened as the near term contracts quickly increased. As the curve flattens and returns to normal it presents several opportunities. The trade we suggest called a spread swap is similar to a call calendar spread involving selling front month volatility while buying back month volatility.

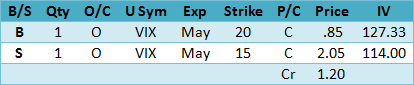

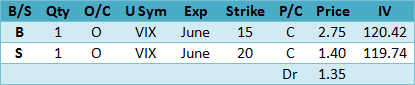

Here is an idea with defined risk to trade a VIX calendar spread without the risk of blowing out the account.

Breaking it down, this involves selling the May 15-20 Call Spread while simultaneously buying the Jun 15-20 Call Spread.

First the May,

Now the June,

Buying the VIX Jun/May 15-20 Call Spread Swap for .15.

Since the VIX does not trade like stocks, there is a possibility the front month could expire much higher than the back month. With this in mind, we know our risk on this trade is 5.00 or 500 per 1 lot while the potential reward is 4.85 or 485 per 1 lot. However, a loss would incur if the front month increased substantially something that has not happened in a long time. Presuming the return to a normal term structure, this trade is profitable, when the May futures decline faster than the June futures.

The VIX trade suggestion from a few weeks ago, along with updates from the last two weeks, remains suspended until SPX closes below the trigger at 1538.57. If it does, we expect to see the front month, which is most likely to be May, increase rapidly as the futures curve flattens again. Consider a long call perhaps in combination with a short put as described in the previous Digest issues above.

IVOLopps? Takeover File

Although there have been few recent takeovers generating much enthusiasm in the options market, here is one with both increasing options volume and implied volatility that is worth considering for those with a longer time horizon.

Sprint Nextel Corp. (S)

Just when it seemed that Softbank was about to complete a takeover and restructuring, another bid came in from Dish Network Corp. (DISH) that seems to have the support of some large shareholders, but not the bondholders thereby increasing the uncertainty as reflected in the rising options implied volatility.

The current Historical Volatility is 39.94 and 20.91 using the Parkinson’s range method compared to 15.60 and 16.37 last month before DISH, with Implied Volatility Index Mean of 29.39 up from 25.05 last week and 14.42 one month ago. The IV/HV ratio is .74 and 1.41 using the range method to calculate the HV. Friday’s put-call ratio at .20 was very bullish while the volume was 23,633 contracts traded compared to the 5-day average volume of a whopping 305,880 contracts.

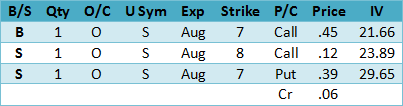

Since we think it will likely take some time for a final resolution and the stock price will most likely not fluctuate very much with the market, here is an August suggestion.

?

?

While there is some implied volatility edge in the short put, the risk here is both interested parties withdraw from the bidding and the stock declines back to 6 or below, which means assignment of stock at 7 and lower implied volatility reducing the attractiveness of subsequent call sales. However, should the stock close at 8 on expiration the gain would be about 65% based upon regular margin requirements. Setting a SU (stop/unwind) will not likely help to limit the risk if the bidding ends since the stock could drop significantly. Therefore, the only real effective risk management strategy is to limit the position size.

The suggestions above use the Friday closing middle price between the bid and ask. Monday, the option prices will be somewhat different due to the time decay over the weekend and any price change.

?

Summary

The combination of continuing deterioration of market breadth along with the recent liquidation in the e-mini S&P 500 Futures increases the risk that the correction will turn lower once again, perhaps after one more upswing forming the right shoulder of a Head & Shoulders Top.