It has been quite awhile since suggesting more than one takeover idea; perhaps there will be more to come.

International Game Technology?(IGT) ?up 1.51 the world’s largest slot machine maker advanced last Monday when they announced hiring Morgan Stanley to find a buyer and by the end of the week it advanced 3.35 on unusually high volume as at least two interested groups emerged.

The current?Historical Volatility?is 50.89 and 37.71 using the?Parkinson’s range method, with an?Implied Volatility Index Mean?of 62.77 up from 25.99 the week before. The 52-week high was 62.77 Friday while the low was 24.47 on May 23, 2013. The implied volatility/historical volatility ratio using the range method is 1.66 so the option prices are expensive relative to movement of the stock but less relevant if more takeover bids are forthcoming. The?put-call ratio?at .11 reflects bullish call activity while Friday’s volume at 107,658 contracts traded compares to the 5-day average volume of 40,740 contracts. The bid/ask spreads seem reasonable. Here is long theta put sale idea

?![]()

With good volatility edge, use a close back below 14 as the?SU?(stop/unwind).

Cree, Inc.?(CREE) the LED bulb maker selling at 49 times trailing twelve month earnings and 25 time forward earnings and continually rumored to be takeover candidate was up 2.37 Friday on news that perhaps General Electric (GE) or Koninkijke Philips (PHG) may once again have an interest.

The current?Historical Volatility?is 22.91 and 25.55 using the?Parkinson’s range method, with an?Implied Volatility Index Mean?of 34.07 up from 29.63 the week before. The 52-week high was 63.05 on October 13, 2013 while the low was 29.33 on June 10, 2014. The implied volatility/historical volatility ratio using the range method is 1.33 so the option prices are slightly expensive relative to movement of the stock. The?put-call ratio?at .10 reflects bullish call activity while Friday’s volume at 47,947 contracts traded compares to the 5-day average volume of 14,100 contracts. Here is another long theta put sale idea.

![]()

With slight volatility edge, use a close back below 45 as the?SU?(stop/unwind).

Dish Network Corp.?(DISH) although more likely to be an acquirer there was no specific news accounting for increasing implied volatility Friday. It could just be responding to other activity in the communications sector or perhaps there will be news released later this week. In the current low implied volatility environment we will take what we can find. Here is another put sale idea.

The current?Historical Volatility?is 22.63 and 26.36 using the?Parkinson’s range method, with an?Implied Volatility Index Mean?of 37.59 up from 34.28 the week before. The 52-week high was 52.06 on May 2, 2014 while the low was 27.55 on March 21, 2014. The implied volatility/historical volatility ratio using the range method is 1.43 so the option prices are slightly expensive relative to movement of the stock. The?put-call ratio?at .35 is bullish while Friday’s volume at 44,308 contracts traded compares to the 5-day average volume of 12,940 contracts.

![]()

With some volatility edge the bid/ask spread is wider so be careful and see if it can be narrowed somewhat. For the?SU?(stop/unwind) use a close back below the pivot made May 22 at 57.21.

T-Mobile US, Inc.?(TMUS) 32.91 as a follow-on to the put sale suggested in?Digest Issue 22 “Liquidity & Dividends”?here is another along with updated options data.

Since a regulatory decision is not expected soon, implied volatility is likely to remain high for some time providing opportunities to sell more option premium.

The current?Historical Volatility?is 20.26 and 21.87 using the?Parkinson’s range method, with an?Implied Volatility Index Mean?of 33.84 down from 35.61 the week before. The implied volatility/historical volatility ratio using the range method is 1.54 so the option prices are expensive relative to movement of the stock but near the lower part of the 52 week range. Friday’s option volume was low at 2,312 contracts traded compared to the 5-day average volume of 4,880 contracts.

![]()

In the event of an adverse FCC or Justice Department ruling, be prepared to take the stock by assignment if it closes below 32 on the July expiration, but a ruling seems unlikely before the July options expire.

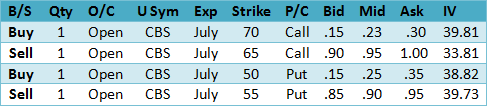

CBS Corporation?(CBS) 60.45 while caught up in the M&A activity this one is better categorized as a reorganization since they are spinning off their 81% ownership in CBS Outdoor Americas (CBSO) through an exchange offer that is expected to be tax-free for participating shareholders in the U.S. However, there was also news Friday they along with others, held preliminary talks with Univision that may not produce results due to a reported high asking price.

Since the stock price is near the middle of a well-defined range, we have a suggestion using a different positive theta strategy.

The current?Historical Volatility?is 21.57 and 20.17 using the?Parkinson’s range method, with an?Implied Volatility Index Mean?of 36.57 down from 38.17 the week before. The implied volatility/historical volatility ratio using the range method is 1.81 so the option prices are expensive relative to movement of the stock but near the upper part of the 52 week range. Friday’s option volume was 62,377 contracts traded compared to the 5-day average volume of 110,120 contracts.

Look at this Iron Condor idea, a short out-of-money call spread along with a short out-of-the money put spread.

Using the bid prices for the sales and the ask prices for the buys results in a net credit of 1.10. With some patience, it may be possible to improve the prices by a few cents. The maximum potential credit is 1.10 on a close between 55 and 65. Using the range historical volatility of 20.17 we estimate the short call and put to be beyond one standard deviation, however if the stock price approaches either we suggest using either a long call or put as a hedge. The margin requirement is the maximum risk of 500 and the credit is 110 representing a possible 22% gain in just over one month.

The suggestions above include Friday’s closing middle prices along with the bid/ask. Monday option prices will be somewhat different due to the time decay over the weekend and any price change.

Summary

As expected the S&P 500 Index began retesting the May 13 breakout high of 1902.17 but was supported by favorable M&A news that may also turn the small capitalization and “growth at any price stocks” higher and appears to be exciting options in other stocks creating opportunities. In the meanwhile, there are increasing signs of professional hedging activity so prepare for a further decline by watching key levels of the VIX futures premium and the CBOE S&P 500 Skew Index.