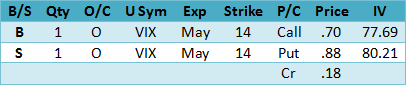

Since the May VIX Futures (VIK3) expire on the opening Wednesday May 22 they are the most responsive to changes in the VIX price. For hedging later in the week and beyond we suggest using options on June VIX Futures (VIM3) 15.08. Remember to match the strike price to the futures not the VIX index.

Since the implied volatility of the VIX options is low relative the historical volatility, as mentioned above a long call position could provide a hedge as the VIX rises with market declines. However, there is still time decay to consider, so adding a short put position creates a synthetic long and offsets most to the time decay and vega risk.

Here are the details based upon the Friday closing prices. Keep in mind hedging when in a well-defined market uptrend is a contrarian strategy and should be used sparingly for specific events and then quickly unwound. Accordingly, here are two ideas, the first for Monday and Tuesday this week.

?

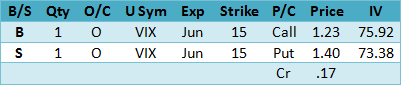

For selective hedges later in the week and beyond, here is another with June options.

?

The suggestion above uses the Friday closing middle price between the bid and ask. Monday, the option prices will be somewhat different due to the time decay over the weekend and any price change.

?

Summary

Last week the underlying strength of the equity markets improved dramatically as market breadth confirmed advances in the DJ Transportation Index as broader market indexes advanced to new highs. Although the S&P 500 Index will retest the breakout above 1600 at some point, for now the equity market is quite favorable, so don’t “Sell in May and Go Away” this year.