According to the Aesop fable, once a Countryman possessed the most wonderful Goose imaginable. Every day when he visited the nest, the Goose had laid a beautiful, glittering, golden egg.

He took the eggs to market and soon became rich. However, before long he grew impatient because she gave him only a single golden egg a day. He was not getting rich fast enough.

Then one day, after he had finished counting his money, an idea came to him that he could get all the golden eggs at once by killing the Goose and cutting it open. When done, he did not find the source of the eggs and his precious Goose was dead.

Those who have plenty want more and lose all they have.

Last week, we proposed that the IPO stampede along with rotation out of “growth at any price stocks” could trigger a broader market decline, one that is now well underway.

Market Review

S&P 500 Index?(SPX) ?Last Monday’s range was lower than projected implying the market was weaker than expected on increasing volume. Then after attempting a rebound Wednesday, the decline resumed Thursday and Friday. For the week, the loss was 49.40 points or 2.65%.

The operative upward sloping trendline line from the June 24, 2013 low now crosses at 1795.12, just 1.13% lower, making a likely target this week. The last two times the upward sloping trendline was tested, it failed to hold the decline, but then reversed higher within a few days. Presuming a similar pattern for this decline, look for support around or just below 1795. In the event that fails, the next stop will be the February 5 low at 1737.92 and since the momentum is still down a test of 1795 is quite likely.

CBOE Volatility Index??(VIX) ?After two weeks of complacency, VIX seems to have awoken Thursday and Friday.

The table below shows the VIX cash compared to the next two futures contracts as well as our calculation of Larry McMillan’s day-weighted average between the first and second months.

The day weighting applies 10% to April and 90% to May for an average premium of -2.23% shown above. Our alternative volume-weighted average between April and May, regularly found in the Options Data Analysis section on our homepage, is slightly higher at -1.61%. We consider premiums less than 10% to be cautionary while the premiums for a normal term structure are 10% to 20%. Last week the premiums were positive but less than 10 % every day except Friday when they closed at -1.61%. While we associate negative premiums with market turns, they can be negative for several days. For example, on the last market decline the premiums were negative for almost two weeks reaching -11.44% two days before the reversal on February 5, when the premium was -4.80%. Based upon this we suspect there will be several more days of negative premiums before the market turns higher.

VIX Options

With a current 30-day?Historical Volatility?of 112.33 and 88.58 using?Parkinson’s range method, the table below shows the Implied Volatility (IV) of the at-the-money VIX calls and puts using the futures prices based upon Friday’s closing option mid prices along with their respective month’s futures prices, since the options are priced from the tradable futures.

Comparing to the range historical volatility of 88.58 implies overpriced April options with just two trading days before expiration while the May options are less expensive. Reflecting the rush for portfolio protection Friday?s volume was 1,032,406 contracts compared to the weekly average of 671,840 contracts.

CBOE S&P 500 Skew Index?(SKEW) 122.59. SKEW measures the purchase of out-of-the-money S&P 500 Index puts that require a very large downside move to profit from long put positions. An increase of this index indicates greater expectations for an extreme down move.

On Friday March 14, SKEW suddenly declined 15 points closing at 112.66 taking it back down near the May 28, 2013 low of 112.47. Then the next Monday it advanced 30.61 to 143.27 making a 52-week high. We suspected a data problem, however if correct the close is once again just under the mid-point of the range in neutral territory. In the past, high readings have been associated with market tops presumably due to portfolio managers purchasing out-of-the-money puts for insurance while they are inexpensive.

US Dollar Index?(DX) ?The dollar was trending slightly higher until April 4 reaching 80.42 before abruptly turning lower as Treasury interest rates declined renewing expectations for a slowing global economy after China?s recent trade balance report. This would be consistent with increasing gold prices last week.

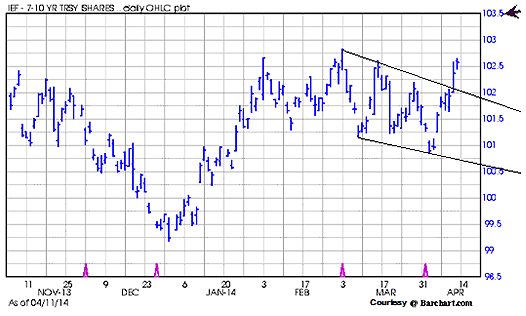

iShares Barclays 7-10 Year Treasury ETF?(IEF) ?The previous potential Head & Shoulders Top identified in March?remains possible until it closes back above the March 3 high at 102.83. However, the current operative technical pattern appears to be a declining wedge with an upside measuring objective at 103.68, which would eliminate the previous potential Head & Shoulders Top. If so, the interest rate yield would be back down to the June 19, 2013 level of 2.31%. Here is the chart with an arrowhead indicating the area of the measuring objective equating to a yield of about 2.31%.

While declining interest rates would usually suggest a weaker economy the other possibility of funds coming out of equities and temporarily seeking safe haven in Treasuries is just as likely since crude oil prices remain high. IEF continues to be one of the more important indicators to be watching since it provides some clues as to where the equity sale proceeds may be going.

iShares Dow Jones Transportation Average Index?(IYT) ?The transports are no longer suggesting “all aboard” as they were last week?and are now casting doubt on expectations for a cyclical rotation into economically sensitive sectors. Watch the upward sloping trendline from the June 24, 2013 low of 106.32 that now crosses at 128.47, just 2.34% lower for confirmation of a slowing economy, as the railroads now seem to imply.

NYSE McClellan Summation Index?The summation index is an intermediate indicator comprised of a running total of the McClellan oscillator, a leading indicator, which is the difference between a 19 period and a 39 period exponential moving average of the net difference between the advancing and declining issues on the New York Stock Exchange.

Since our last review, the summation index declined 51.35 points with a 120.23-point decline last week as could be expected with the market decline.