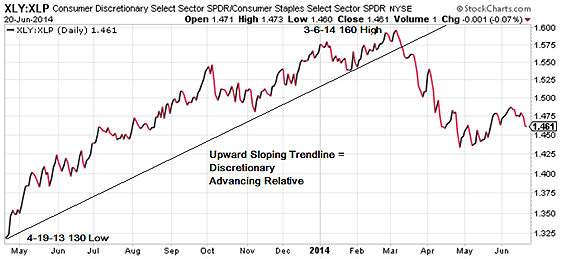

One way to investigate sector rotation is to compare the?Consumer Discretionary Select Sector SPDR ETF?(XLY) ?to the?Consumer Staples Select Sector SPDR ETF?(XLP). Dividing the discretionary index by the stapes creates a comparative ratio helping to identify the relative flow of funds into these sectors. The discretionary sector usually performs better in the later stages of market cycles while the stapes perform best during early contraction. In practice, it’s more complicated since sector performance may be contradictory like now. Here is the chart.

From the low at 130 on April 19, 2013 until the top at 160 on March 6, 2014 discretionary outperformed staples before suddenly declining in early March until early May when discretionary made an attempt to rebound. However, on June 9 at 1.49 it again turned lower as crude oil advanced 1.65 basis August futures closing at 103.59, now 106.83 confirming concerns that higher crude oil prices are likely to depress discretionary spending.

Normally the rotation out of discretionary into safer consumer staples is a sign of a weaker market but that has not been the situation to date as the transports continue to be strong. However, if crude oil continues higher to challenge 110 or beyond the transports could also be in for trouble.

Crude Oil WTI? basis August futures has been in backwardation, when the near term futures are priced higher than the deferred, for 24 weeks now at 2.98. Backwardation is usually associated with inventory shortages, which appears to be the current situation as inventory accumulates on the gulf coast leaving a shortage at the Cushing WTI delivery point. Adding fuel to the fire last week the Commitment of Traders report revealed Large Speculators increased their net long position by 39,145 contracts to 457,156 as open interest expanded 62,286 contracts to 2.28 million.

While some may consider the current crude oil price unsustainable and attempt to fade the advance remember the situation in Iraq gives longs the justification for their record long speculative futures positions and since cash crude was 110.54 September 2, 2013 and as high as 113.93 in early 2011, these could be the Large Speculator’s targets.

United States Oil?(USO) until there is a clear breakdown in price we suggest remaining long?USO since crude oil remains in backwardation adding some positive carry to the ETF using futures and this is seasonally the time when crude oil is relatively strong. A long August 40/43 call spread around .55 should be about right with a?SU(stop/unwind) on a close below support at 38, just in case.

The suggestion above uses the closing middle prices between the Friday bid and ask. Monday option prices will be somewhat different due to the time decay over the weekend and any price change.