Cyclical Rotation Review

While the market decline is even beginning to cast some doubt on the rotation into cyclicals, crude oil prices remain high.

Checking WTI crude oil prices we notice they went into backwardation in the first week of January and Friday reached at high of -3.23 basis May – August, that is May futures were 103.74 while August were lower at 100.51, backward to normal carry trade by 3.23. This suggests low inventories at the Cushing Oklahoma delivery point for CME futures while there appears to be plenty of supply at the refineries on the Gulf coast.

Since USO uses futures that are now in backwardation every time they roll over the near term contract they pick up some carry. For example assuming they rolled the contracts Friday they would have sold May for 103.74 and bought June at 102.62, for a gain of 1.12 or 1.08%. While it has been in backwardation for 14 weeks, there is no assurance it will remain. In addition, crude oil basis May futures and USO both appear to be testing early February highs so there could be some double top risk.

Here are two ideas, the first assumes the double top and lower prices while the second has it going into new high ground – not good for the transports or the economy.

United States Oil?(USO)?

First the option details,

The current?Historical Volatility?is 16.92 and 11.62 using the?Parkinson’s range method, with an?Implied Volatility Index Mean?of 16.99, up from 16.97 the week before. The 52-week high was 28.16 on August 28, 2013 while the low was 13.66 on December 26, 2013. The implied volatility/historical volatility ratio using the range method is 1.46 so the option prices are high relative to movement of the ETF but below the midpoint of the 52 week range. The?put-call ratio?at 1.10 is bearish, but not surprising as this ETF is a hedging favorite for long oil stock positions. Friday’s volume was 49,115 contracts traded compared to the 5-day average volume of 34,090 contracts so there is reasonable options liquidity.

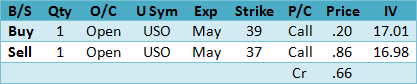

Here is a call credit spread idea assuming a double top.

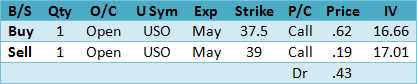

Now the bullish breakout idea,

The trend, slight volatility and futures rollover edge goes to the bull call spread but it has the double top risk so use a close back below 37 as the?SU?(stop/unwind).

The suggestions above use the closing middle prices between the Friday bid and ask. Monday option prices will be somewhat different due to the time decay over the weekend and any price change.

Summary

It appears rotation out of “growth at any price stocks” along with an oversupply of IPOs, is killing the goose that lays golden eggs. Since the downside momentum is accelerating, expect to see lower lows over the next week or two while watching the S&P 500 Index upward sloping trendline at 1795 for support.