What Happened To The U.S. Natural Gas Glut?

Today’s Spotlight Market

This past Thursday, the Energy Information Administration (EIA) released its weekly Gas storage report and the numbers were historic. 250 billion cubic feet (bcf) of Gas was drawn from storage during the week ending February 14th, which was the 4th consecutive week of a 200 bcf plus draw. Gas inventories have fallen to their lowest levels in February since 2004.

Although current Gas inventories are becoming tight, many traders are looking at the recent price rally to initiate short positions in more distant contract months in anticipation of increased Gas production due to higher prices, which makes Gas drilling more profitable for more marginal producers. While this would seem to be a logical theory, we must consider the possibility that the U.S. could also face a warmer than average summer, which would trigger an increase in Gas usage for cooling and potentially prevent adequate amounts of Gas to be placed in storage prior to the start of next winter?s heating season. If this were to occur, we could see Gas prices closer to the levels seen back in the mid to late 2000?s, when prices of $4 were viewed as a floor and not a ceiling.?? ?

Fundamentals

The ?sleepy? Natural Gas market of the past 2 years is a thing of the past, as an unusually harsh winter for most of the U.S. has caused Natural Gas demand to soar. Natural Gas is the main fuel used for heating for nearly half of U.S. households, and this season?s cold and snowy weather has taken a huge bite out of U.S. Gas inventories. The most recent EIA Gas storage report shows U.S. Gas inventories falling to 1.443 trillion cubic feet (tcf) for the week ending February 14th. This is over 1 tcf below last year?s totals, and nearly 34% below the 5-year average.?

With Gas storage levels becoming tight, the market has seen aggressive buying by both speculators and end-users have emerged, particularly for the lead month March futures, which is normally the last ?unofficial? month of the winter heating season. In the last month, the March futures have gained over $2, and the notoriously volatile Mar/Apr spread, known in the trade as the ?widow maker?, has moved to a $1.25 March premium vs. a $0.25 March premium less than 2 weeks ago.??

Although higher overall prices for Natural Gas should encourage increased production in the coming months, especially once frozen wells have thawed, in the near-term, weather forecasts calling for another bout of arctic cold for the eastern and central parts of the U.S. through the beginning of March could see traders continue to buy near-term futures, particularly the April contract, once the March futures expires on Wednesday.

Technical Notes? -? View Today’s Chart

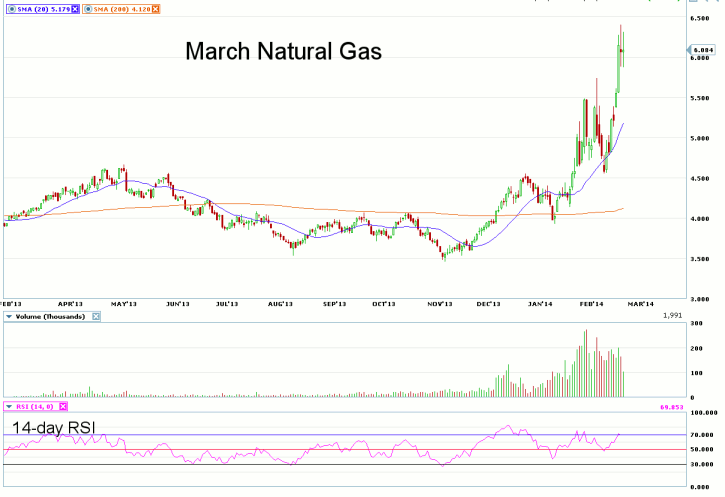

Looking at the daily chart for March Natural Gas, we notice prices went parabolic last week, moving nearly $1 in just three trading sessions. Prices seem to have found some resistance at 6.400, as some good selling has emerged near this price level. Option traders have been aggressive in the out-of-the-money March calls, as a spike in implied volatility triggered short-covering buying in strikes ranging from $7 to $10 last week, despite these options having less than a week left before expiration, with the futures trading near $6. ?Rich? premiums for these options have lured some premium sellers into the Natural Gas options market that would not normally have an interest in this product. This should make for interesting options expiration on Tuesday, as market participants position themselves for a potentially ?interesting? trading session on Wednesday when the March futures go off the board.? The 6.400 price level remains as resistance for the March futures, with support found near 5.500.???

——————————————————————————————-

Disclaimers

This article is provided for informational purposes only. No statement in this article should be construed as a recommendation to buy or sell a security or to provide investment advice. The content provided has been obtained from sources deemed reliable but is not guaranteed as to accuracy and completeness. optionsXpress makes every effort to provide timely information to its recipients but cannot guarantee specific delivery times due to factors beyond our control.

Derivatives involve substantial risk and are not appropriate for all investors. Please read the?“Disclosure Statement for Futures and Options”?prior to investing in futures or options.

For investments using a straddle or strangle options strategy the potential loss is unlimited. Multi-leg option strategies are subject to multiple commissions. Profits may be eroded by the commission expended to open and close the positions and?other risks?apply.

??