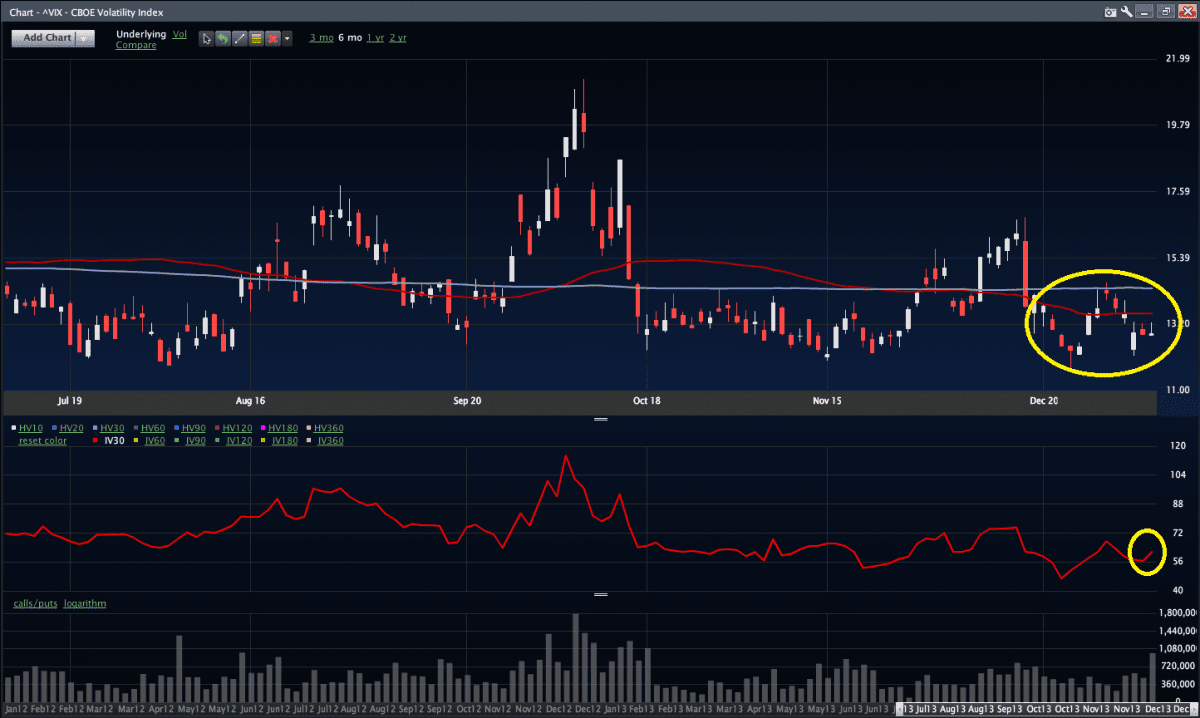

Last week we wrote how we expected the ATM straddle to go out somewhere near 18 dollars into non-farm payrolls. ?Boy were we off. ?Yesterday, the straddle went out less than 12.00. ?This means that the market is about 58% certain (greater than 50/50) that the SPX is going to move less than 12 dollars tomorrow. ?The VIX and the Vol of VIX both failed to catch any bid this week.

Livevol (R)?www.livevol.com

If anything, this week the market has crushed movement expectations. ?Optoins in SPX have been sold, ?options on VIX have been sold down. ?Vol has been killed basically everywhere. ?The question is, ?was the sale justified? ?The answer is yes and no. ?I am willing to bet that the the vol sale makes sense in relation to tomorrow, but not in relation to news that is going to be coming out over the next few weeks. ?With taper on the table CPI is going to start driving interest rates and data is going to be scrutinized every where. ?It can’t be too good and can’t be too bad either. ?Basically, ?the VIX in the mid 12’s is probably a buy.

The Trade:

We continue to think straddles are under priced and skew is expensive. ?We like broken wing butterflies and straddles. ?We are less in love with back spreads despite the low vol. ?Skew is bid everywhere, we like risk reversals vs straight long plays. ?Non-farms should be ‘bought with,’ ?meaning the trend is your friend today. ?If the market sells off, it will keep doing so, and vice versa.

Sign up for our one day class: ?Trading in a Bear Market