While we had previously suggested preparing for a more extensive pull back the market strength last week seems to have reduced the necessity for employing more hedging strategies. Further, we will close our IWM put spread that we opened when IWM briefly closed below 90 on April 18. While we continue to favor special situations, the larger capitalization stocks with good liquidity and dividends are leading the market higher.

iShares Russell 2000 Index (IWM)

For the trade plan implemented on April 18 we originally set the SU (stop/ unwind) at a close back above 95, however we no longer see any reason to risk a further decline. Therefore, we will close the put spread now even though the broader market indexes may continue lagging the large capitalization stocks, since it looks as if the recent pull back is over. Confirmation will come when SPX closes above the April 11 high of 1597.35

iShares MSCI Japan Index (EWJ)

The uptrend mentioned seven weeks ago continues as more information arrives about the stimulus actions underway in Japan. Although it is widely acknowledged the yen will decline the G-20 has apparently agreed to go along with program hoping it may help stimulate other economies in the process. In the meanwhile, those waiting for a pullback could be disappointed as overbought EWJ continues higher with only slight retreats. Since there is a good chance this condition could continue for awhile longer, we suggest adding a call spread to the position.

First, an option data update.

The current Historical Volatility is 20.43 and 8.76 using the Parkinson’s range method. The unusual disparity between the historical volatility measures is a function of the narrow daily trading ranges around the fixed closing price of the previous day’s Nikkei 225. The Implied Volatility Index Mean is 19.48, up slightly from last week at 19.15, but up substantially from 14.84 last month. The IV/HV ratio is .95 and 2.22 using the range method to calculate the HV. Friday’s put-call ratio at .15 was extremely bullish while the volume was 13,100 contracts traded compared to the 5-day average volume of 34,590.

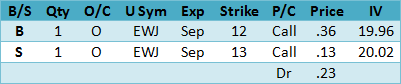

Consider this long call spread.

?

?

We suggest using a close back below the upward sloping trendline now at 10.75 as the SU (stop/unwind). Considering the current uptrend, we think it could reach 13 by the September options expiration in 145 days. If so, the spread would be worth the width between the strike prices, or 1.00 less the debit of .23 for a .77 gain, which is 3.3 times the amount at risk.

The suggestion above uses the Friday closing middle price between the bid and ask. Monday, the option prices will be somewhat different due to the time decay over the weekend and any price change.

?

Summary

Last week’s advance by the major equity indexes increased the chances that the recent pull back has run its course and the uptrend is about to resume its ascent to new highs.